Not sure if you should invest in a retirement annuity (RA), tax-free savings account (TFSA) or discretionary investment for retirement?

Where to invest savings for optimal growth and tax efficiency remains the top priority for most investors when they seek professional financial planning advice. The majority select a RA as the most logical option for their needs. However, this might not always be their best or only option.

Saving for retirement through retirement annuities and preservation funds has always been widely recommended due to the tax benefits available. Investors are entitled to a tax deduction on their contributions of up to 27.5% of their taxable income or remuneration but limited to a maximum of R350 000. Growth on the investment is further free of any capital gains or dividend withholding tax implications – the objective being to encourage investors to save towards their retirement to avoid them ultimately becoming dependent on government support. Controversial legislation, designed to protect investors, has however resulted in poor performance over several years and as an unintended consequence made the assets held by investors in these products vulnerable to governmental decision making.

Regulation 28 of the Pension Funds Act prescribes and limits pension monies to 75% equity exposure, listed property to 25% and offshore exposure to 30%. This composition is generally reflected in balanced unit trust funds and has been a popular choice for pension monies where the asset manager ensures compliance with Regulation 28. Most of these funds hold around 40% in South African equities. The returns from the JSE have, however, been extremely poor by global comparison in the long term.

The JSE All Share Index delivered 7.76% over the past five years which explains the poor average performance of Regulation 28 compliant balanced funds. In sharp contrast, the S&P 500 and the MSCI World Index has delivered 17.71% and 16.32% respectively.

Source: Allan Gray Fund research

The downside of investing in a product such as a discretionary investment, which is not subject to Regulation 28 of the Pension Funds Act, is the liability towards interest, dividend and capital gains tax earned on the investment.

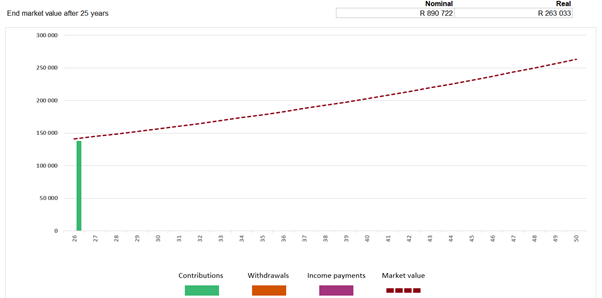

Let us compare the following scenario of a younger investor:

Investor 25 years of age wanting to retire at the age of 50 (25 years to retirement).

| Investment amount | R137 500 |

| Retirement Annuity growth rate | 7.76% |

| Discretionary investment growth rate average | 17.02% (17.71% + 16.32%/2 as per paragraph 3 above) |

| Salary | R500 000 (Marginal tax rate of 36%) |

| Inflation | 5% |

| Term | 25 years |

Source: Allan Gray Financial Planning

Capital at the end of the term in nominal terms:

| Retirement Annuity | Discretionary Investment | |

| Initial amount invested | R137 500 (27.50%) | R137 500 |

| Amount at 50 | R890 722 | R6 995 279 |

| Growth | R753 222 | R6 857 779 |

| Tax saving | R45 370 | |

| CGT payable | R987 520 (40% x 36%) | |

| Capital at the age of 50 with tax break | R936 092 | |

| Capital at 50 after CGT | R6 007 759 |

The difference between investing in a discretionary investment and investing in a RA, which is subject to Regulation 28 of the Pension Funds Act, is R5 071 667.

Let us compare the same scenario but for an older investor:

Investor 54 years of age wanting to retire at the age of 55 (1 year to retirement).

| Investment amount | R137 500 (27.50% x R500 000) |

| Retirement Annuity growth rate | 7.76% |

| Discretionary investment growth rate | 17.02% (11.33% + 14.25%/2) |

| Salary | R500 000 (Marginal tax rate of 36%) |

| Inflation | 5% |

| Term | 1 Year |

Source: Allan Gray Financial Planning

Capital at the end of the term in Nominal terms:

| Retirement Annuity | Discretionary Investment | |

| Initial amount invested | R137 500 | R137 500 |

| Amount at 55 | R148 170 | R160 903 |

| Growth | R10 670 | R23 403 |

| Tax saving | R45 370 | |

| CGT payable | R3 370 (40% X36%) | |

| Capital at 55 with tax break | R193 540 | |

| Capital at 55 after CGT | N/A | R157 533 |

The difference between investing in a RA at an older age and investing in a discretionary investment is R36 007 – making a RA the more attractive alternative.

Investors who are invested in a retirement product may retire from their investment from the age of 55 and transfer the proceeds to a living annuity (LA). A LA is governed by the Income Tax Act, as such the restrictive provisions of Regulation 28 as contained in the Pension Fund act is not applicable to these investment products – thus allowing investors to obtain up to 100% offshore exposure and generate similar levels of returns as possible in a discretionary investment.

Conclusion:

Younger investors who invested in a discretionary investment would have received significant larger returns when they retire compared to other younger investors who invested in a RA for purposes of receiving tax relief.

If you are an older investor who can retire from a RA within a year, a RA will be more beneficial but only if the capital is transferred to a living annuity thereafter in order to obtain similar levels of growth compared to a discretionary investment.

Whether an investor is younger or older, they should however make use of a TFSA and contribute the maximum allowable amount each year which is currently R36 000 for the 2022 tax year.

The TFSA will allow an investor to invest 100% offshore to generate similar returns to that of a discretionary investment but without the need to pay any tax on the growth.

If you want to make contributions for the current tax year, do not delay. To ensure that a company can report your contributions to a RA or TFSa during the 2022 tax year to Sars, the contribution amount must reflect in the company’s bank account on February 28.

It should be noted that each investor has different needs, objectives, and risk profiles and as such the same advice will not always apply to everyone. It is advisable to always consult an accredited, qualified financial planner to devise a plan best suited to the investor’s personal circumstances and financial goals.

Read more about retirement planning and tax planning.