By Stefan Janse van Vuuren – Brenthurst Wealth

The product allows for capital to compound without any future capital gains tax implications.

Very rarely does a single investment secure an individual’s financial security, but rather a collective of investments each playing a role as part of an overall financial plan. When used correctly, a tax-free savings account (TFSA) can be a vital cog in that plan.

TFSAs have been underutilised by investors since their introduction in 2015. To their detriment, as the product allows for capital to compound without any future capital gains tax implications. Unfortunately, many investors make the mistake of opening a TFSA at their bank. TFSAs opened at major banks are mostly invested in money market instruments, the asset class which provides a sense of security but the least amount of long-term capital growth. It would be in the investor’s best interest to rather open a TFSA at any of the leading platforms in South Africa that allows the investor to invest in equities – the asset class which has proved to provide superior capital growth over the long term.

Importantly, investors must understand the role of the product in their overall financial plan. The benefits are negated if the capital is not left to compound for as long as possible – we are not talking months or years but decades. You don’t have to take my advice, but please lend your ears to legendary investor Charlie Munger, who iterates this by saying “the first rule of compounding is to never interrupt it unnecessarily”.

A vital part of investors due diligence is to familiarise themselves with the product’s rules before investing. An individual only has R500 000 lifetime allowance and R36 000 per year (R3 000pm). If investors exceed these allowances, they face tax penalties. Once capital is withdrawn from a TFSA, it is not possible to recover any part of that allowance. Further reasons for investors to avoid dipping into their capital at all costs.

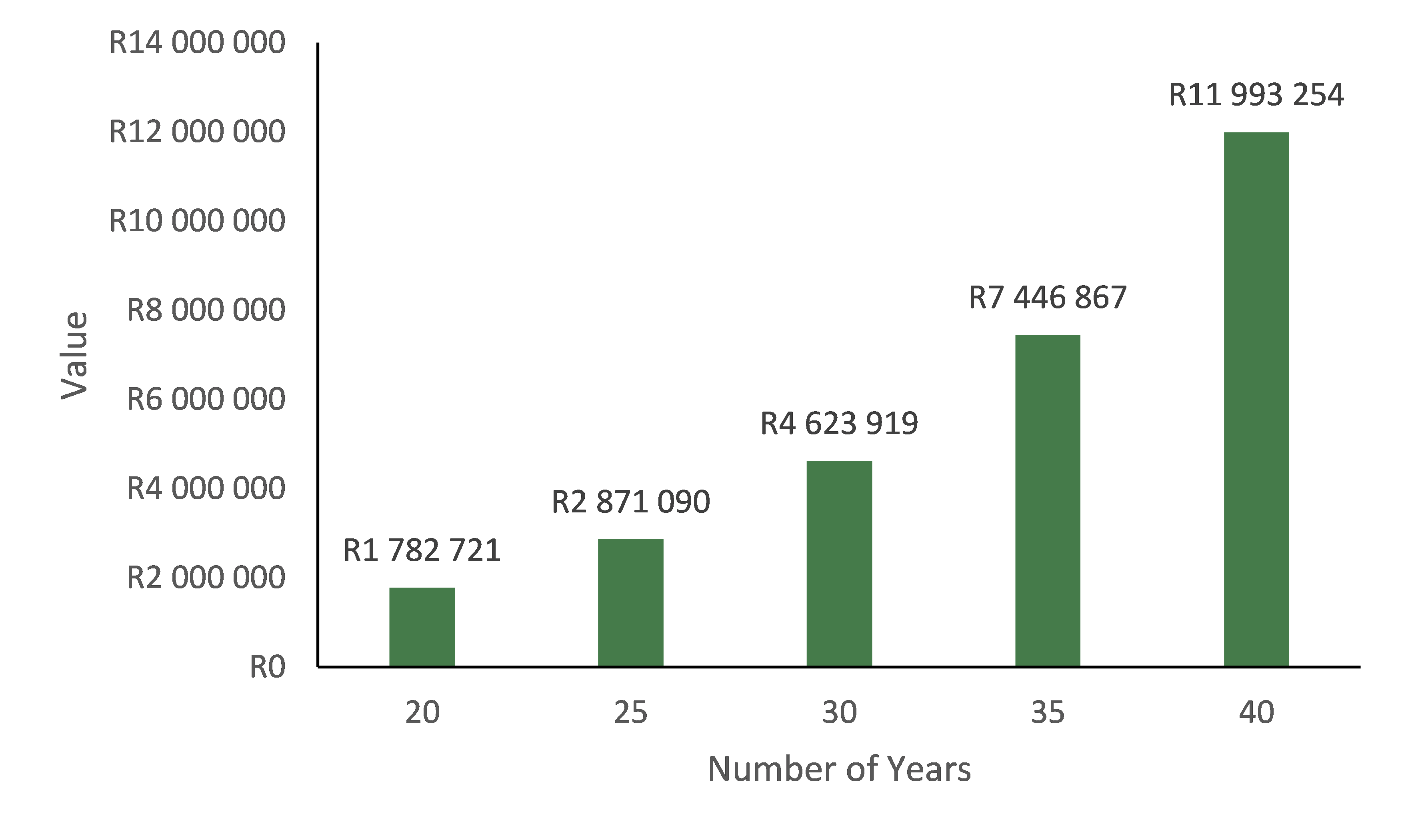

The graph below not only shows the compounding effect, but the tax savings (at 30% tax rate) if invested in a TFSA (10% pa growth, 50/50 split in investment return between interest and capital gain, R36 000 per year contribution until R500 000 limit reached).

Source: Ninety One

The goal would be to fully utilise the R500 000 allowance as soon as possible (i.e., maximising the R36 000 per annum each year), and then leave the capital to compound for as long as possible. Due to the benefits of a TFSA only being realised if left to compound for the long-term, the product is especially beneficial for younger generations.

Young professionals should seriously consider saving R3 000 per month in a TFSA and not a retirement annuity (RA). TFSAs have no limit on offshore exposure and if needed, the capital can be accessed before the age of 55. RAs limit offshore exposure to 30% and the capital cannot be accessed until 55.

Another example of efficient use of TFSAs is parents contributing to TFSAs in their children’s names. This is only advised if spending the money can be deferred for as long as possible. If not (e.g., saving for tertiary education) rather open a normal discretionary investment in the child’s name or a TFSA in one of the parents’ names, so as not to misuse a child’s R500 000 lifetime allowance. Children are not liable for tax until they start earning an income, therefore opening a discretionary investment, and keeping their R500 000 allowance intact could prove effective.

Source: Brenthurst Wealth

The above graph is a continuation of the first graph, showing the power of compounding if given sufficient time – free of tax as a reward for self-discipline and patience.